South Korea’s biggest cryptocurrency exchange, Upbit, could be hit with a fine of $34 billion - the largest regulatory penalty ever proposed against a crypto platform in history. This isn’t a rumor. It’s a real, documented enforcement action taken by the Financial Services Commission (FSC) in early 2025. The reason? Systemic failures in customer identification, or KYC, that put millions of users at risk and broke the country’s financial laws.

What Exactly Went Wrong?

Upbit, launched in 2017 by Dunamu, handles over $8 billion in trades every single day. It’s not just big in Korea - it’s among the top six crypto exchanges worldwide. But size didn’t protect it from scrutiny. In late 2024, regulators conducting routine license reviews found between 500,000 and 700,000 cases where customer IDs were improperly verified. These weren’t minor mistakes. Investigators saw ID documents with blurred faces, mismatched names, fake photos, and even photos of people who clearly weren’t the account holders. Under South Korea’s Special Financial Transactions Act, every failed KYC check is a standalone violation. And each one can carry a fine of up to 100 million Korean won - about $68,500. Multiply that by half a million violations, and you get the staggering $34 billion figure. But it wasn’t just about bad ID checks. Upbit also traded with overseas platforms that weren’t registered in Korea. That’s a direct violation of anti-money laundering (AML) rules. The exchange didn’t just fail to verify its own users - it also didn’t check who it was doing business with. That’s like running a bank that doesn’t ask for ID from customers or verify who they’re sending money to.What Did the Regulators Do?

On January 20, 2025, the Financial Intelligence Unit (FIU) gave Upbit a deadline to respond to the findings. By January 21, the FSC made its final decision. On February 25, Dunamu, Upbit’s parent company, received official notice. The punishment wasn’t the full $34 billion - and experts agree it never would have been. But the actual penalties were still severe. Upbit was forced to stop accepting new deposits and withdrawals for three months. Existing users could still trade, but no new accounts could be opened. If regulators had gone all the way, Upbit would’ve had to freeze new registrations for six months. This wasn’t just a slap on the wrist. It was a signal to the entire crypto industry: no matter how big you are, if you break the rules, you’ll pay.Why Does This Matter Beyond Korea?

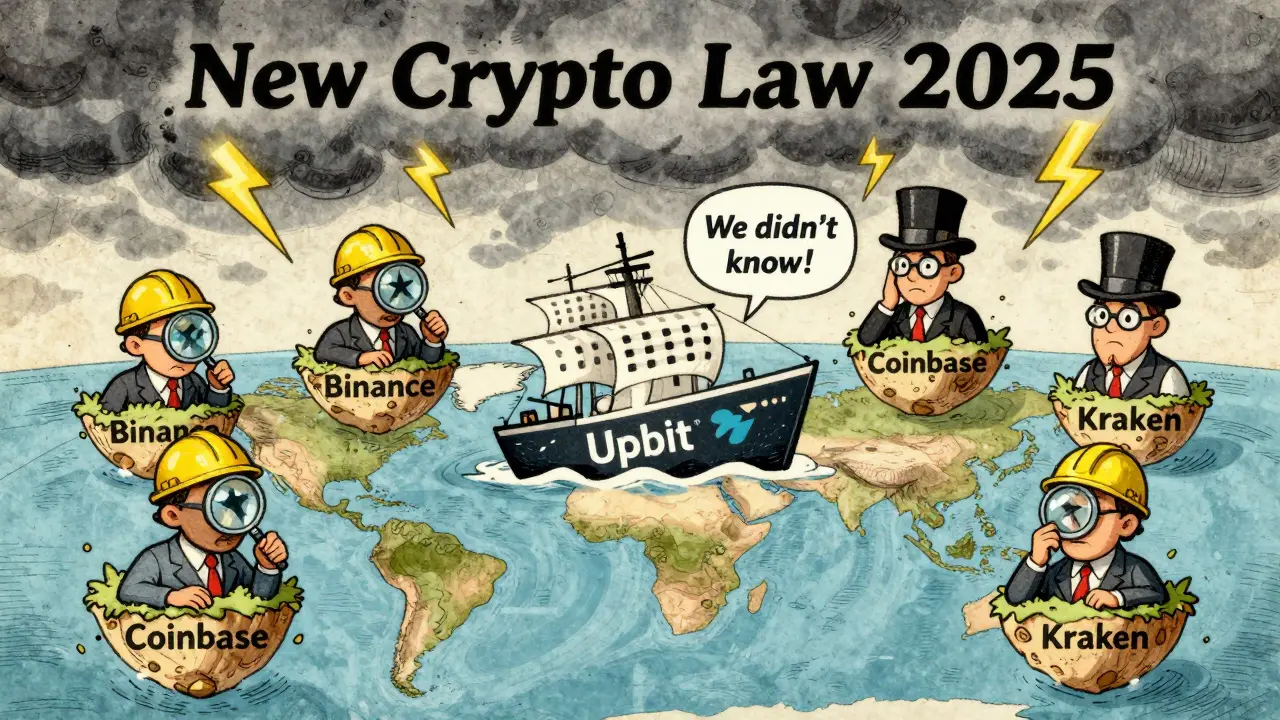

Upbit isn’t just a Korean company - it’s a global player. Its size means its actions ripple across markets. When a platform this large fails KYC, it opens the door for money laundering, fraud, and tax evasion. Regulators in the U.S., EU, Japan, and Singapore all took notice. Exchanges in other countries started auditing their own systems. Some paused new user onboarding to review their ID verification processes. Others upgraded to AI-powered facial recognition and document authentication tools. The Upbit case became a textbook example of what happens when compliance is treated as an afterthought. It also exposed a deeper problem: many crypto platforms operate in legal gray zones. Upbit claimed it didn’t know which overseas exchanges were registered because blockchain transactions are anonymous. That’s not a valid excuse. Regulators don’t care if it’s hard - they care if you tried. If you’re running a financial service, you’re responsible for knowing who you’re dealing with.

What’s the Bigger Picture?

South Korea has been tightening its crypto rules for years. The Upbit case wasn’t an accident - it was the result of a deliberate shift. In 2025, the government moved fast to draft its first comprehensive crypto law. The goal? To make Korea a leader in regulated digital asset markets, not a haven for wild west trading. This crackdown wasn’t isolated. In February 2025, police arrested a major crypto scammer known as ‘Jon Bur Kim’ for stealing $48 million using a fake token called Artube. Special crypto crime units were formed. Banks were ordered to report suspicious crypto transactions. The message was clear: crypto isn’t lawless. It’s now part of the financial system - and it’s being treated like one.How Did Upbit Respond?

Upbit didn’t deny the violations. Instead, they said the failures were unintentional. They claimed it was hard to track overseas platforms because blockchain doesn’t have a central registry. That’s true - but it’s also irrelevant. Other exchanges found ways to comply. Binance, Kraken, and Coinbase all have global KYC systems that work across borders. Upbit didn’t invest in the same infrastructure. The company promised to fix things. They hired compliance officers from major banks. They installed new AI tools to detect fake IDs. They started requiring video verification for all new users. They even began auditing their partner exchanges. But the damage was done. Trust took a hit. Trading volume dropped 22% in the first quarter of 2025.

What’s the Real Fine?

The $34 billion number is a legal maximum - a number used to show how serious the violations were. Experts believe the actual fine will be closer to $1-2 billion. That’s still the largest crypto fine ever. But the real cost isn’t the money. It’s the lost time, the reputational damage, and the forced overhaul of their entire business model. Other exchanges are now spending millions on compliance. They’re hiring former regulators. They’re running internal audits every month. They’re training staff to spot red flags. The cost of compliance has gone up - but the cost of ignoring it just went up even more.What This Means for You

If you trade on any crypto exchange, this case affects you. Why? Because it proves regulators are watching. If your exchange fails KYC, they can shut it down. Your funds could be frozen. Your trades could be halted. No warning. No grace period. It also means better protection. Exchanges that invest in real compliance are less likely to be hacked, less likely to be used for scams, and less likely to disappear overnight. Upbit’s failure made the entire industry safer - by showing what happens when you cut corners.What’s Next?

Upbit is still under review. Regulators are doing on-site inspections to make sure the fixes are real. They’re checking if the new AI tools actually work. They’re testing whether staff can identify fake documents. The license renewal process is ongoing. Meanwhile, South Korea’s new crypto law is expected to pass by late 2025. It will require all exchanges to register with the FSC, submit monthly compliance reports, and use government-approved KYC tools. Non-compliant platforms will be banned from operating in Korea. This isn’t just about Upbit. It’s about the future of crypto. The days of “move fast and break things” are over. The new rule is: build with compliance from day one - or don’t build at all.Why is the fine $34 billion if Upbit didn’t pay that much?

The $34 billion is the theoretical maximum based on 500,000+ individual violations, each carrying a fine of up to $68,500. It’s a legal tool used to show the scale of the failures. Regulators don’t intend to impose the full amount - but they use it to send a strong message. Actual fines are expected to be between $1-2 billion, still the largest in crypto history.

Did Upbit shut down completely?

No. Upbit was only blocked from processing new deposits and withdrawals for three months. Existing users could still trade crypto among themselves. The exchange never stopped operations - but it lost new customers and faced heavy scrutiny during its license renewal.

Are other Korean exchanges in trouble too?

Yes. Regulators launched audits across all major Korean exchanges after Upbit’s case. Bithumb, Korbit, and Coinone were all asked to submit compliance reports. Some were fined smaller amounts for minor KYC gaps. But none came close to Upbit’s scale of violations.

Can a crypto exchange survive a major fine like this?

Yes - if they act fast. Upbit survived by overhauling its compliance team, investing in AI verification tools, and cooperating fully with regulators. Many exchanges that faced smaller fines in the U.S. and Europe also recovered. The key is transparency and speed. Denial or delay makes things worse.

Is this just a Korea thing, or does it affect me if I’m not in Korea?

It affects everyone. Upbit is one of the world’s largest exchanges. Its failure forced global platforms to tighten their own KYC rules. If you trade on Binance, Coinbase, or Kraken, you’ve likely seen stricter ID checks since 2025. This case raised the global standard for compliance - and that’s good for users.

Comments (21)

Shawn Roberts

This is wild but also so predictable 😅 Crypto’s been a free-for-all for too long. Glad someone’s finally holding the big guys accountable.

Daniel Verreault

upbit really thought they could just wing it like its 2017? bro they had 8bil in daily volume and still used basic id checks?? lmao

prashant choudhari

The $34 billion figure is a legal construct not a financial penalty. Each failed KYC is treated as a separate violation under South Korean law. This is standard procedure for systemic non-compliance.

Jake West

Oh wow a crypto exchange got caught doing the bare minimum? Shocking. Next they’ll tell us the sky is blue and water is wet. Who even uses Upbit anymore?

surendra meena

This is why crypto is doomed!!! They’re coming for us ALL!!! They’ll freeze your wallet next!! They’ll track your dog’s blockchain transactions!! I told you this would happen!!!

Mike Pontillo

So they fined them for not checking IDs? And you’re surprised? People think crypto is magic money. It’s not. It’s finance. And finance has rules.

Jordan Fowles

The real question isn’t the fine. It’s whether regulators can enforce compliance without crushing innovation. There’s a line between safety and suffocation. We’re dancing near it.

Elisabeth Rigo Andrews

Upbit’s failure isn’t unique. It’s symptomatic. The entire industry treated KYC as a checkbox. Now they’re paying the cost of technical debt. The real tragedy? Users paid too.

rachael deal

Honestly? This is good news for everyone who actually wants to use crypto responsibly. No more sketchy platforms. No more rug pulls hiding behind anonymity. We needed this.

Mandy McDonald Hodge

i just hope they dont overdo it now... like make everyone do 10 min video calls just to buy btc... i get it but its getting ridiculous 😅

Bruce Morrison

Compliance isn’t optional anymore. If you’re handling money, you’re a financial institution. Period. Upbit’s mistake was thinking the rules didn’t apply to them. They were wrong.

nayan keshari

You call this a crackdown? Wait till they start taxing crypto gains at 70%. Then you’ll see real pain. This is just warmup. The real axe is coming.

alvin mislang

If you’re not doing KYC, you’re a criminal. No excuses. No ‘blockchain is anonymous’ nonsense. If you run a business, you follow the law. Period. 🙄

Adam Hull

The $34B figure is performative. It’s theater. Regulators know they’ll never collect it. But it serves a purpose: scare the rest into compliance. Psychological leverage. Classic.

Joydeep Malati Das

The global impact is undeniable. Exchanges outside Korea have upgraded systems, hired compliance officers, and increased audit frequency. This is a watershed moment for the industry’s maturation.

Steve Williams

This is what responsible innovation looks like. Not ignoring regulations. Not hiding behind decentralization. Building with integrity from day one. Upbit failed. Others learned.

Monty Burn

The real cost isn't the fine it's the loss of trust. People don't care about the numbers they care about whether their money is safe. Upbit broke that. And that's harder to fix than any system

Andrew Prince

Let me be clear: the FSC’s approach is not merely regulatory-it is epistemological. The very ontology of decentralized finance is being reconfigured through the imposition of centralized compliance infrastructure. The blockchain, once a symbol of autonomy, is now being subsumed under the bureaucratic apparatus of the nation-state. This is not progress. It is colonization.

Kenneth Mclaren

This is all a distraction. The real story? The FSC is working with the CIA to track crypto users. That’s why they picked Upbit. They want to build a global surveillance network. You think this is about KYC? No. It’s about control.

Brandon Woodard

The regulatory framework in South Korea is not punitive-it is corrective. The $34 billion figure is a statutory ceiling designed to incentivize systemic reform. The actual penalty reflects proportionality, not vengeance. This is governance, not retribution.

Abhisekh Chakraborty

I’m just saying... if they shut down Upbit completely, where will I trade my dog coins? 😭 I have 3 million of them and they’re all locked in there. This is the end of the world.