Buying Bitcoin or minting an NFT in India used to be a gray area. Now, it is one of the most heavily regulated spaces in the world. If you hold Virtual Digital Assets (VDAs), every transaction matters. The government isn't just watching; they are taxing every gain at a flat 30%. Miss a deadline, ignore the TDS rules, or fail to report correctly, and your profits vanish faster than a rug pull.

This guide cuts through the noise. It explains exactly how the Indian taxation framework for cryptocurrencies introduced in 2022 works today. You will learn what counts as a VDA, how to calculate your tax liability, why losses don't help you, and how the new Income Tax Act of 2025 changes the game. Whether you are a casual holder or an active trader, getting this right protects your wallet.

What Exactly Is a Virtual Digital Asset?

You might think "crypto" means only Bitcoin or Ethereum. The Indian law sees it differently. Under Section 2(47A) of the Income Tax Act, 1961, a Virtual Digital Asset is defined as any information, code, number, or token generated through cryptographic means that represents value digitally.

This definition is broad. It includes:

- Cryptocurrencies like Bitcoin (BTC) and Ether (ETH).

- Non-Fungible Tokens (NFTs).

- Utility tokens from DeFi protocols.

- Any digital representation of value exchanged with consideration.

It explicitly excludes Indian Rupees and foreign fiat currencies. So, if you trade USDT for INR, that is not a VDA transaction. But if you swap BTC for ETH, that is two separate taxable events. This distinction trips up many investors who assume swapping coins is just moving money around. In India, it is a sale.

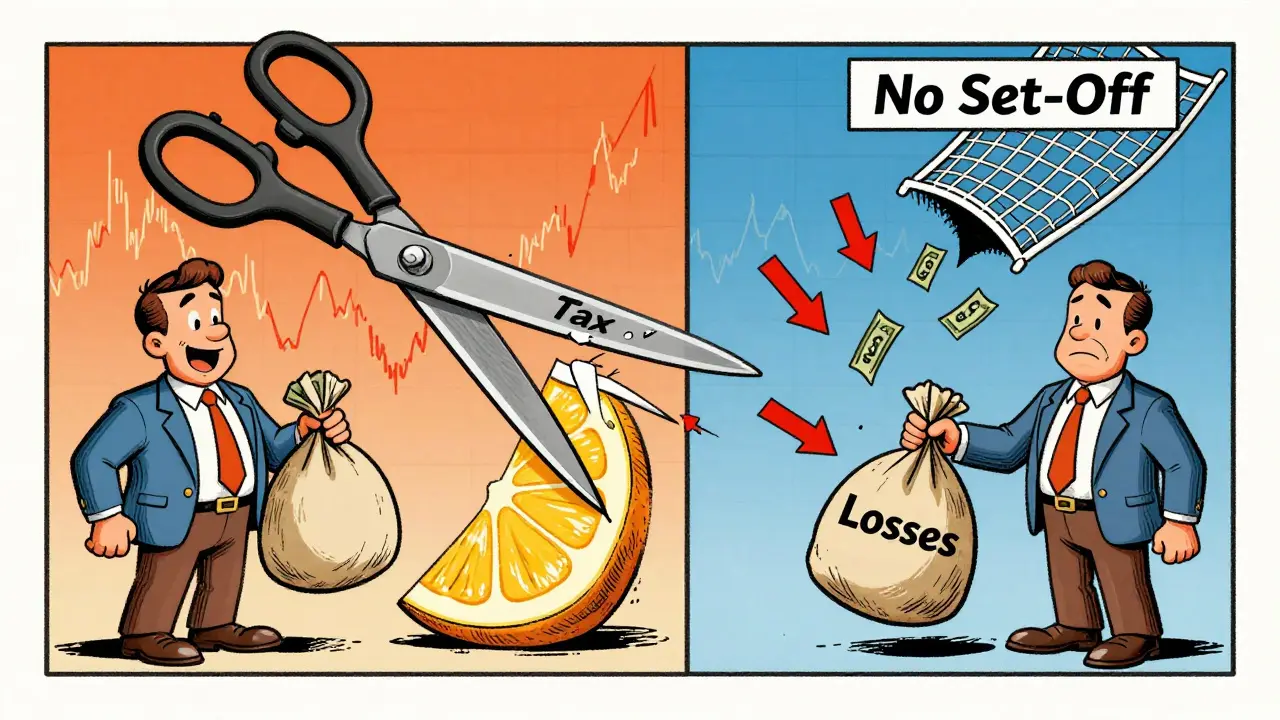

The 30% Flat Tax Rate Explained

Here is the core rule: all gains from VDAs are taxed at a flat 30% under Section 115BBH. This applies regardless of your income slab. If you earn ₹5 lakh a year or ₹5 crore a year, the rate is the same. There is no benefit for holding assets long-term. Short-term capital gains and long-term capital gains are treated identically.

Let’s look at the math. Suppose you buy 1 BTC for ₹80 lakhs and sell it for ₹100 lakhs. Your profit is ₹20 lakhs. You pay 30% on that profit, which is ₹6 lakhs. Add the 4% health and education cess, and your total tax bill is ₹6.24 lakhs. That leaves you with ₹13.76 lakhs net.

Crucially, you can only deduct the cost of acquisition. Transaction fees, gas fees, mining electricity costs, and storage expenses are not deductible. Many traders expect to offset these operational costs against their profits, but the law does not allow it. This makes the effective tax burden higher than it appears on paper.

Why Losses Cannot Be Set Off

This is where many investors lose sleep. In traditional equity markets, if you lose money on one stock, you can set that loss against profits from another stock. With VDAs, this is impossible. Losses from virtual assets cannot be set off against salary income, business income, or even gains from other VDAs in the same year.

Imagine you make ₹10 lakh profit on Bitcoin but lose ₹8 lakh on Ethereum. You still pay 30% tax on the full ₹10 lakh Bitcoin gain. The ₹8 lakh Ethereum loss is not ignored entirely, but it offers no immediate relief. You can carry forward this loss for eight years to offset future VDA gains. However, if you never make more VDA gains in those eight years, that loss expires worthless.

This rule creates a asymmetric risk profile. Upside is taxed heavily, downside provides limited protection. Professional traders often find this structure punitive because it eliminates the ability to smooth out volatility through tax planning.

TDS Rules: The 1% Deduction Mechanism

To ensure compliance, the government mandated a 1% Tax Deducted at Source (TDS) on VDA transactions. This applies when you transfer a VDA to another person. The threshold depends on who is receiving the asset.

| Recipient Type | Annual Threshold | TDS Rate |

|---|---|---|

| Specified Person | ₹50,000 | 1% |

| Non-Specified Person | ₹10,000 | 1% |

| No PAN Provided | Any Amount | 20% |

A "specified person" is someone whose turnover exceeds ₹1 crore or professional receipts exceed ₹50 lakhs in the previous year. For everyone else, the limit is ₹10,000 annually. Once you cross this limit in a financial year, every subsequent transaction triggers a 1% deduction.

If the recipient does not provide a Permanent Account Number (PAN), the TDS rate jumps to 20%. This is a massive penalty designed to force KYC compliance. Note that Section 206AB, which previously imposed higher TDS for non-filers, was omitted effective April 1, 2025. This simplifies the landscape slightly, but the 20% rate for missing PAN remains a critical trap.

Filing Returns: Schedule VDA

When you file your Income Tax Return, you must use ITR-2 or ITR-3 forms. Inside these forms, you will find Schedule VDA. This section requires detailed disclosure of every VDA transaction.

You need to report:

- Date of acquisition.

- Date of transfer.

- Cost of acquisition in INR.

- Full value of consideration received in INR.

For crypto-to-crypto swaps, you must convert values to INR using exchange rates from notified platforms like CoinDCX or WazirX at the time of transaction. Keeping records is vital. The National Institute of Securities Markets (NISM) reports that 65% of tax disputes stem from inadequate record-keeping. Save your wallet addresses, transaction hashes, and exchange statements. Do not rely on memory.

Impact of the Income Tax Act, 2025

The regulatory landscape shifted again with the Income Tax Act, 2025, which received presidential assent in August 2025. While the 30% tax rate remains unchanged, the administration has evolved.

The Act introduces the concept of a "Tax Year" replacing the traditional financial year for assessment purposes. It also emphasizes digital-first enforcement. The Central Board of Direct Taxes (CBDT) has launched specialized dispute resolution channels for VDA cases. This suggests the government is preparing for a surge in litigation as taxpayers challenge valuation methods.

Finance Minister Nirmala Sitharaman stated in her budget speech that the framework aims to balance innovation with revenue protection, targeting 15% annual growth in VDA tax revenue through 2030. This indicates the regime is here to stay. Expect stricter audits and automated data matching between exchanges and tax authorities.

Practical Strategies for Compliance

Navigating this system requires discipline. Here are actionable steps to stay compliant:

- Track Every Swap: Treat every crypto-to-crypto trade as a taxable event. Use portfolio tracking software that integrates with Indian exchanges.

- Maintain INR Records: Convert all values to INR at the time of transaction. Do not use end-of-year averages.

- Verify TDS Certificates: Check Form 16E issued by exchanges. Errors in TDS calculation are common, with Trustpilot reviews citing over-deduction issues.

- Carry Forward Losses: Document losses meticulously. Even though they cannot be set off now, they may reduce taxes in future years.

- Consult a CA: Given the complexity, hiring a Chartered Accountant familiar with VDA rules can save thousands in penalties.

Some investors explore gifting assets to family members in lower tax brackets. However, gift tax implications and clubbing provisions must be considered. Another strategy involves Bitcoin ETFs, which may be taxed as securities rather than VDAs, potentially offering different treatment. Always verify current SEBI guidelines before adopting such strategies.

Is staking income taxed differently than trading gains?

Yes. Staking rewards are typically treated as income from other sources and taxed at your applicable slab rate upon receipt. When you later sell the staked tokens, the difference between the fair market value at receipt and the selling price is taxed as a VDA gain at 30%. This double taxation layer makes staking less attractive for some investors.

Can I claim deductions for mining equipment?

No. The law explicitly disallows deductions for incidental expenses related to VDA transactions. Mining hardware costs, electricity, and maintenance cannot be deducted against VDA gains. However, if mining is conducted as a business, some expenses might be claimed under business income heads, but the subsequent sale of mined coins still attracts 30% VDA tax.

What happens if I forget to report a small transaction?

Failure to report VDA transactions can lead to scrutiny notices from the Income Tax Department. Penalties include interest on delayed payment and potential fines under section 270A for concealment of income. Given the automated data sharing between exchanges and tax authorities, unreported transactions are increasingly detected during routine assessments.

Does the 30% tax apply to NFT sales?

Yes. NFTs fall under the definition of Virtual Digital Assets. Any profit made from selling an NFT is subject to the 30% flat tax rate. The cost basis is the amount paid to acquire the NFT, including marketplace fees if explicitly allowed by specific circulars, though generally only acquisition cost is deductible.

How do I handle crypto received as payment for services?

Crypto received as payment is first taxed as professional or business income at your slab rate based on its fair market value on the day of receipt. When you eventually sell or transfer that crypto, the difference between its current value and the value at receipt is taxed as a VDA gain at 30%. This results in dual taxation.