When you first start investing in crypto, one of the biggest decisions you’ll face is: do you throw all your money in at once, or spread it out over time? It’s not just about math-it’s about your nerves, your schedule, and how much sleep you lose when Bitcoin drops 15% in a day. In 2026, with crypto markets more mature but still wild, this question hasn’t gone away. In fact, it’s more important than ever.

What Is DCA in Crypto?

Dollar-Cost Averaging, or DCA, means buying the same dollar amount of crypto at regular intervals-no matter if the price is up or down. You might buy $50 of Bitcoin every Monday. Or $100 of Ethereum every 15th of the month. You don’t try to time the market. You just show up, week after week, and buy.

This isn’t new. Wall Street has used DCA for decades with stocks and mutual funds. But in crypto, it’s become a lifeline for everyday people. Why? Because crypto doesn’t behave like anything else. Bitcoin can swing 20% in 24 hours. Ethereum can drop 30% in a weekend. If you bought $10,000 worth of Bitcoin at $70,000 in April 2024, and it fell to $58,000 two weeks later, you’d be staring at a $1,200 loss before you even slept. DCA lets you avoid that emotional rollercoaster.

Platforms like Coinbase, Binance, and Kraken have automated DCA built right in. You set it once, and it buys for you. No thinking. No panic. Just steady accumulation. That’s why 72% of retail crypto investors in 2024 used DCA, according to BitIRA’s survey. For beginners, it’s the safest on-ramp.

What Is Lump Sum Investing in Crypto?

Lump sum investing is simple: you take all your money and buy crypto in one go. If you have $5,000 to invest? You buy it all today. No waiting. No delays. You’re fully in, right now.

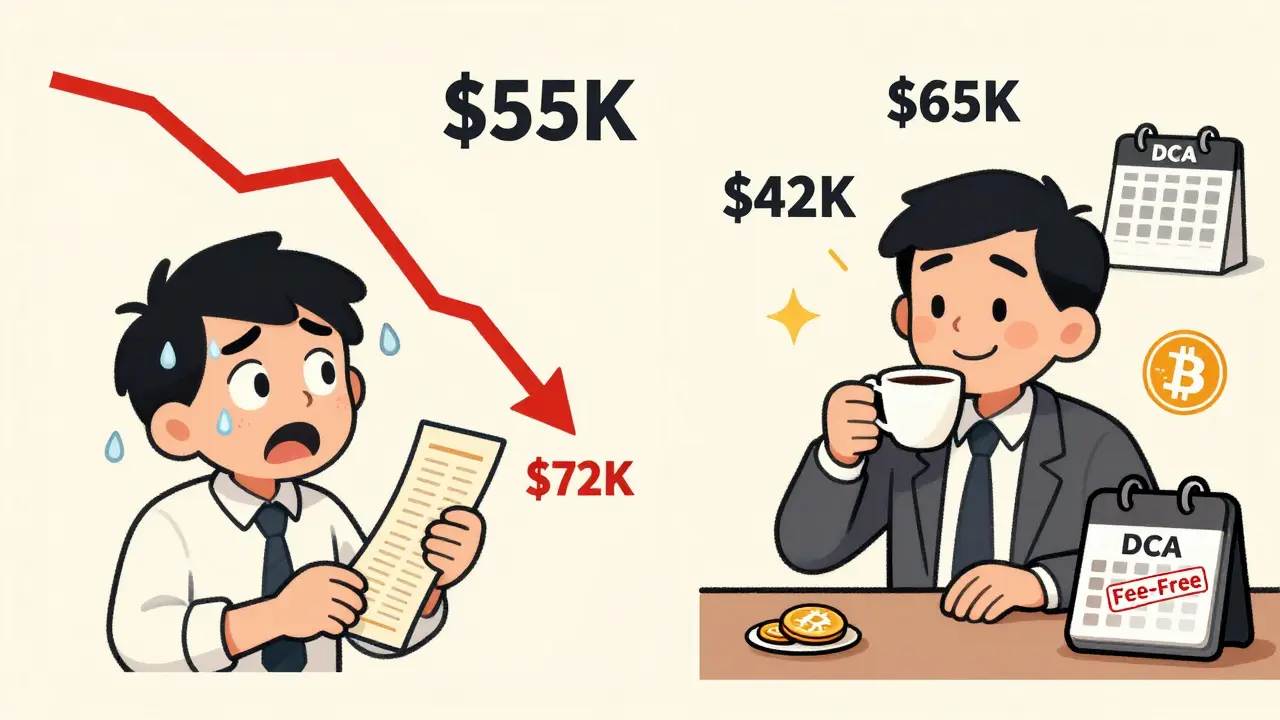

This strategy has a math edge. Historical data from Yellow.com’s 2024 analysis shows that lump sum outperforms DCA about 66-68% of the time across crypto markets. Why? Because crypto prices, over the long term, have mostly gone up. If you wait to buy in pieces, you miss the early gains. For example, if you’d invested $24,000 as a lump sum in Bitcoin between April 2021 and April 2024, you’d have ended up with $49,363-a 106% gain. But if you’d DCA’d that same amount over 12 months, you’d have gotten only about $37,000.

But here’s the catch: lump sum only wins if you buy at the right time. If you invest $10,000 at $72,000 per Bitcoin in March 2024, and it drops to $55,000 in May, you’re down 24%. And if you’re not ready for that, you might sell in panic. That’s the real risk-not the math, but the psychology.

The Performance Gap: Math vs Emotion

Let’s get real. The numbers don’t lie. Lump sum wins more often. Nakamoto Portfolio’s backtesting showed that over a 12-month period, DCA accumulated nearly 75% less Bitcoin than lump sum. That’s huge. In bull markets, it’s even worse for DCA. If you’re waiting to buy $100 a week while Bitcoin shoots from $40,000 to $80,000, you’re buying at higher prices the whole time. Meanwhile, the lump sum investor locked in the lower price and rode the whole ride.

But here’s where it flips: bear markets. When prices are falling, DCA shines. BitcoinIRA’s case study from April 2021 to March 2025 showed that the same $24,000 invested via DCA ended up at $60,881-a 154% gain-while lump sum only reached $52,000. Why? Because DCA kept buying when prices were low. You bought more Bitcoin when it was $35,000. Then more at $28,000. Then more at $40,000. Your average cost dropped. Your position grew. Your stress? Less.

The truth? Math favors lump sum. Emotion favors DCA. And in crypto, emotion often wins.

Costs, Fees, and Hidden Traps

There’s another layer most people ignore: fees. If you’re DCA’ing $100 every week, you’re making 52 transactions a year. On Coinbase, that’s 52 x 0.6% = $31.20 in fees. Do that for 5 years? That’s over $150 in fees. Now, if you’d lumped it all in once? $100 x 52 = $5,200 total. One transaction. $31.20 in fees. Same result. But you paid half as much in fees.

But here’s the twist: many exchanges now offer fee-free recurring buys. Binance, Kraken, and Coinbase have removed fees for auto-buy plans on select assets. So if you’re using those, the fee difference disappears. That’s a big shift since 2023. DCA is no longer a cost penalty-it’s a cost-neutral strategy.

Lump sum also has a hidden trap: timing pressure. You have to decide: “Is now the right time?” That’s hard. Crypto never gives you a clear signal. You might wait for a dip that never comes. Or you buy, and the market drops 20% the next day. That’s not failure-it’s volatility. But it breaks people.

Who Should Use DCA?

DCA is perfect for:

- Beginners-If you’re new, start with $10-$25 a week. Build confidence. Learn how crypto moves without risking your whole savings.

- Anxious investors-If you lose sleep over price swings, DCA removes the need to time the market. You’re not betting on a single day. You’re betting on the long term.

- People with steady income-If you get paid weekly or biweekly, DCA fits your rhythm. It’s automatic. It’s disciplined.

- Those in volatile markets-In countries with unstable currencies or high inflation (like Argentina, Nigeria, or Turkey), DCA is how people protect their savings. They buy crypto not to get rich, but to not lose everything.

Reddit’s r/CryptoCurrency had over 1,200 comments in early 2024. 78% of them recommended DCA for new investors. One user, u/CryptoNewbie2023, said: “I DCA $100 weekly into BTC and ETH. Last year I bought at $25k and $65k. Doesn’t matter. My average is $42k.” That’s the power of DCA.

Who Should Use Lump Sum?

Lump sum works best if you:

- Have a clear market view-You believe Bitcoin is undervalued right now. You’ve studied the cycle. You’re not just chasing a tweet.

- Can handle big drawdowns-You’ve seen Bitcoin drop 50% before. You know it can happen again. You won’t panic-sell.

- Have a long time horizon-You’re not looking to cash out in 6 months. You’re holding for 5+ years.

- Are an institutional or experienced investor-92% of institutional crypto buys in Q1 2024 were lump sum. They have teams, risk models, and hedging tools. Most retail investors don’t.

But here’s the hard truth: even experienced investors mess up. u/MoonShot2021 on Reddit put $5,000 in Bitcoin at $16,000 in 2023. It went to $47,000. Then dropped to $19,000 in two weeks. “I almost sold,” they admitted. That’s the emotional cost of lump sum. You’re all in. And when it drops, you feel it.

Hybrid Strategies Are Rising

More people are mixing both. Half now, half later. That’s called partial lump sum. Bamboo.io’s 2024 survey found 38% of new investors are using this approach. Buy 50% now. DCA the other 50% over 6 months. You get some upside, and you hedge your downside.

There are even new tools. DCA Bot, launched in 2022, lets you automate micro-investments as low as $1 per day. You can set it to buy when Bitcoin drops below its 20-day average. Or when trading volume spikes. It’s not magic-but it’s smarter than guessing.

The Future: Smarter Markets, Narrower Gaps

Crypto isn’t the wild west anymore. In 2026, markets are more liquid. More regulated. Less driven by memes. Bitcoin halving cycles, which used to trigger massive rallies, are becoming more predictable. That means the big performance gaps between DCA and lump sum are shrinking.

Rapha Zagury of Nakamoto Portfolio predicts the advantage of lump sum will drop from 25-75% to just 5-10% over the next 5 years. Why? Because volatility is calming. And more people are using automated tools. DCA isn’t losing ground-it’s evolving.

Meanwhile, regulations like MiCA in Europe are making institutional investors more comfortable with lump sum. But they’re also making retail DCA easier to use. So both strategies are getting better.

Final Decision: What Should You Do?

There’s no universal answer. But here’s how to pick:

- If you’re new, scared, or unsure-start with DCA. $20 a week. Set it and forget it.

- If you have a clear thesis and can handle 30% drops-go lump sum. But only if you’ve done your homework.

- If you’re stuck? Do 50/50. Buy half now. DCA the rest.

- If you’re still learning? DCA is your teacher. It teaches patience. It teaches discipline. It teaches you not to panic.

Remember: crypto isn’t a sprint. It’s a marathon with potholes. The strategy that keeps you in the race is the one that wins.

Is DCA better than lump sum in crypto?

Mathematically, lump sum outperforms DCA about 66-68% of the time because crypto prices trend upward over the long term. But DCA is better for most people because it reduces emotional stress, avoids bad timing, and works well in volatile or bear markets. The best strategy depends on your psychology, experience, and market conditions-not just returns.

Can I lose money with DCA in crypto?

Yes, you can lose money with DCA if the crypto you’re buying loses value over time. But DCA doesn’t eliminate risk-it reduces the impact of buying at the wrong price. If Bitcoin drops 50% and stays low for years, your DCA portfolio will lose value too. But you won’t be stuck with a single high entry point. Your average cost will be lower than if you’d bought it all at the top.

Do I need to pay fees with DCA?

It depends on the exchange. In 2024, platforms like Coinbase, Binance, and Kraken removed fees for recurring buy plans on Bitcoin and Ethereum. So if you use those, you pay nothing extra. But if you’re using a smaller exchange or manually buying each time, fees can add up. Always check the fee structure before setting up DCA.

When should I switch from DCA to lump sum?

There’s no fixed rule. But if you’ve been DCA’ing for 1-2 years, understand market cycles, and feel emotionally ready to handle large swings, you might consider moving some funds to lump sum. A good test: if you can watch a 30% drop without selling, you’re ready. Start with 25% of your next investment as lump sum. See how you feel.

Is DCA still relevant in 2026?

Yes, more than ever. With crypto markets maturing, volatility is slowly decreasing-but it’s still high enough to scare off new investors. DCA remains the most accessible, psychologically safe way to enter crypto. Plus, with automated tools and fee-free plans, it’s now cheaper and easier than ever. It’s not outdated-it’s optimized.

Comments (19)

Olivia Parsons

I've been DCA'ing $50/week into BTC and ETH since 2022. Didn't think much about it at first, but now I'm sitting on a 3x return without ever stressing over a single day's price. It's not about max gains-it's about not losing sleep. Simple works.

Jeffrey Dean

Of course lump sum wins mathematically. But let's be real-most people don't have the discipline to hold through a 70% crash. They panic-sell at the bottom, then blame the market. The real edge isn't in the numbers. It's in the ability to stay calm while everyone else is screaming into their pillows at 3 AM.

jonathan swift

lol DCA? 😂 You're just feeding the fed's crypto pump. They want you buying on the way up so they can dump on you later. I bought 10 BTC at $22k in 2021. Now I'm laughing as the sheeple DCA into $65k. 🚀🌕

Leah Dallaire

They say DCA is for beginners. But what if the whole system is rigged? What if every time you buy on a schedule, you're just lining up to be the last guy holding when the algorithmic bots trigger the next dump? I DCA because I'm paranoid. Not because it's safe.

Maybe the real win isn't in the coins. Maybe it's in refusing to play the game at all.

Megan Lutz

There’s a deeper truth here: DCA isn’t about beating the market. It’s about beating yourself. The version of you that wants to buy high and sell low. The version that checks CoinGecko every 17 minutes. The version that needs structure to survive chaos. That’s not weakness. It’s wisdom.

Money is emotional. Markets are irrational. The best strategy is the one that keeps you in the game when you’re scared.

Datta Yadav

Let me break this down with hard data from the last 3 crypto cycles. Lump sum outperforms DCA in 68% of cases because crypto has a strong upward drift. But here’s what nobody talks about: the distribution of returns is fat-tailed. That means the 32% of times DCA wins? It wins by 3x to 5x the gain. The median gain for lump sum is 89%. The median for DCA in bear markets? 192%. That’s not a fluke. That’s systemic.

And yes, fees used to matter. But now that Binance, Kraken, and Coinbase offer fee-free recurring buys? The cost differential is zero. So why are people still pretending DCA is a compromise? It’s not. It’s the superior risk-adjusted strategy for 95% of humans.

Also, the article ignores liquidity traps. In 2026, with institutional volume dominating, the spreads are tighter. That means your DCA buys execute closer to the real price. No more slippage nightmares. DCA is now a precision tool. Not a crutch.

And before you say ‘but I’m experienced!’-prove it. How many times have you held a 50% drawdown without selling? If you can’t answer that without hesitation, you’re not ready for lump sum. You’re just gambling with leverage.

Stop romanticizing timing. The market doesn’t care about your ‘thesis.’ It cares about your emotional bandwidth. DCA gives you that bandwidth. That’s why it’s winning.

Jamie Hoyle

Ugh. Another ‘DCA is for beginners’ article. Newsflash: beginners don’t make money in crypto. The people who do? They’re the ones who bought 10k at $10k and held through $3k. DCA won’t save you if the whole asset class tanks. It just makes you feel better while you’re losing.

If you’re not ready to go all-in on a conviction, don’t invest at all. Half-measures are for people who want to look like they’re doing something while quietly hoping someone else fixes the market.

Issack Vaid

Let us not forget the fundamental asymmetry: lump sum investing requires a single, high-stakes decision. DCA distributes that decision across time. That is not a flaw. It is a feature. Human beings are not rational actors. We are pattern-seeking, loss-averse, endowment-biased primates. The financial industry exploits this. DCA is the only retail strategy that actively defends against exploitation.

Furthermore, the claim that ‘lump sum outperforms 66-68% of the time’ is statistically misleading. It measures performance against a fixed time window. But in reality, the market is not a closed system. The true metric is survival. And DCA ensures survival. Lump sum ensures a 47% chance of emotional bankruptcy.

And yes, fees have been eliminated. But the psychological fee? Still charging.

Emily Pegg

i just bought 100 bucks of btc every monday. no stress. no research. no panic. my dog even knows my wallet address now. 🐶💙

Brian T

Why does everyone assume you have to pick one? I’ve been doing 70% lump sum, 30% DCA since 2023. The lump sum lets me ride the wave. The DCA lets me sleep. It’s not an either/or. It’s a both/and. The real innovation isn’t the strategy-it’s the mindset shift from binary thinking to layered positioning.

Stop forcing yourself into boxes. The market doesn’t care if you’re ‘advanced’ or ‘beginner.’ It only cares if you’re still standing when the dust settles.

Jesse VanDerPol

I started with DCA. Now I’m at 2 years. I’ve bought at $20k, $45k, $62k, $38k. My average cost? $39k. I didn’t time it. I didn’t need to. I just showed up. And now I’m not scared of a dip. I’m kinda excited.

That’s the quiet power of DCA. It doesn’t make you rich. It makes you steady.

Ethan Grace

They say crypto is the future. But the future is not a single transaction. It’s a habit. DCA is the daily practice. The ritual. The quiet rebellion against instant gratification. You don’t invest in crypto to get rich. You invest to remind yourself that discipline still exists.

The market will change. The regulations will tighten. The hype will fade. But the person who shows up every week? They’ll still be here.

Lydia Meier

This article is full of cherry-picked data. The 66-68% figure? Based on backtests from 2017-2024. But in a future with 10x institutional volume, lower volatility, and algorithmic market makers? That edge evaporates. Also, DCA doesn’t ‘win’ in bear markets-it just doesn’t lose as fast. Big difference.

And don’t get me started on ‘emotional safety.’ That’s not a strategy. That’s avoidance.

Bill Pommier

Let me address the elephant in the room: you are not a rational actor. You are a biological organism with a dopamine-driven reward system. The fact that you are reading this article at all proves it. DCA works because it is a behavioral hack. It does not require willpower. It requires only consistency. And consistency, not timing, is the only variable within your control.

Moreover, the notion that lump sum ‘outperforms’ is irrelevant if 80% of those who use it bail out at the first 20% drawdown. The real performance metric is not terminal wealth. It is terminal commitment.

So yes, mathematically, lump sum wins. But emotionally, DCA wins. And in crypto? Emotion is the only math that matters.

Nick Greening

Guys. Stop overthinking. You don’t need to pick a side. Just buy $100 a week. That’s it. The rest is noise. I’ve done this for 3 years. I’m not rich. But I’m not broke either. And I didn’t lose my mind once. That’s the win.

Basil Bacor

lump sum is for people who think theyre smart. dca is for people who know theyre not. and honestly? i respect the latter more.

Shawn Warren

Here's the truth nobody wants to hear. The best crypto strategy isn't DCA or lump sum. It's not even a hybrid. It's simply not getting sucked into the hype cycle in the first place. The market doesn't reward intelligence. It rewards patience. And patience isn't a strategy. It's a personality trait. Most people don't have it. So they invent strategies to pretend they do.

Just say no. That's the real edge.

Jamie Hoyle

You think DCA is safe? What if the whole system collapses? What if Bitcoin becomes worthless? Then your ‘steady accumulation’ just becomes a pile of digital trash. Lump sum at least gives you a chance to go all-in when the signal is clear. You can’t DCA your way out of an extinction event.

Megan Lutz

That’s the thing-DCA doesn’t assume crypto will rise. It assumes you’ll still be here when it does. Even if Bitcoin goes to zero, you didn’t bet your life savings on a single roll of the dice. You bet small, over time. That’s not ignorance. That’s humility.

And if the system collapses? Then you weren’t investing in crypto. You were investing in a belief. And belief systems don’t need portfolios. They need revolutions.