Buying a coffee with Bitcoin? Selling half your stash to pay rent? In the eyes of the Internal Revenue Service (IRS), you just triggered a taxable event. It sounds harsh, but it is the reality for millions of Americans holding digital assets. Since March 2014, the IRS has classified Bitcoin and other cryptocurrencies as intangible property rather than currency. This single ruling from Notice 2014-21 is the foundational IRS guidance establishing that virtual currencies are treated as property for federal tax purposes means every trade, sale, or purchase creates a gain or loss calculation.

You might have heard rumors that recent laws like the GENIUS Act changed this. They didn't. As of June 2026, the core rule remains: if you own Bitcoin, you own property. Understanding how this works is not just about avoiding audits; it is about keeping more of your money by managing your tax liability correctly.

The Core Rule: Why Bitcoin Is Property, Not Money

To understand why your taxes look the way they do, you have to look at the definition. When the IRS issued Notice 2014-21, they made a deliberate choice. They did not classify Bitcoin as foreign currency. Instead, they placed it in the bucket of "property."

This distinction matters because currency exchanges usually don't trigger immediate tax consequences for individuals. If you swap Euros for Dollars, you generally don't file a form reporting a gain or loss. But when you swap Bitcoin for Dollars-or even Bitcoin for Ethereum-you are disposing of property. The IRS requires you to calculate the difference between what you paid for that Bitcoin (your basis) and what you received for it (the fair market value). That difference is your gain or loss.

This applies regardless of how you use the asset. Whether you hold it as an investment, use it to run a business, or spend it on personal items, the property classification holds. Even with the passage of the GENIUS Act in July 2025 and ongoing debates around the CLARITY Bill, the IRS has maintained its stance. Regulatory changes affect how banks handle crypto, but they have not altered the fundamental tax code interpretation that Bitcoin is intangible property.

Three Ways You Can Hold Bitcoin

Not all Bitcoin is taxed the same way. Your tax bill depends heavily on how you acquired it and what you plan to do with it. The IRS recognizes three main categories for taxpayers:

- Investment Property: This is the most common category. If you buy Bitcoin hoping its price will go up, it is an investment. Gains here are subject to capital gains tax rates. If you hold it for more than one year, you qualify for lower long-term rates. If you sell within a year, you pay short-term rates, which are higher.

- Business Property: If you mine Bitcoin as part of a trade or business, or if you are a dealer who buys and sells frequently as a primary source of income, your profits may be taxed as ordinary income. This means you pay your standard income tax bracket rate, which can be significantly higher than capital gains rates.

- Personal Property: If you use Bitcoin for personal transactions, like buying goods or services, you still have a taxable event. You must report the gain or loss based on the value of the goods received versus your original cost basis.

Knowing which box you fall into helps you plan. For most casual investors, staying in the "investment" bucket allows you to leverage favorable capital gains rules.

Calculating Gain or Loss: The FIFO vs. Specific ID Debate

Here is where things get tricky. Let's say you bought 1 Bitcoin in 2021 for $30,000 and another in 2024 for $60,000. Today, you sell 1 Bitcoin for $70,000. Which one did you sell?

The IRS wants to know because your tax bill changes drastically depending on the answer. If you sold the 2021 coin, your gain is $40,000 ($70k - $30k). If you sold the 2024 coin, your gain is only $10,000 ($70k - $60k).

You have two methods to determine this:

- Specific Identification: You tell the IRS exactly which coins you sold. This is the best method for minimizing taxes, but it requires impeccable records. You must prove you owned those specific coins and disposed of them. If you can't provide detailed logs showing the transaction history, the IRS will reject this method.

- FIFO (First-In, First-Out): This is the default method if you cannot identify specific lots. The IRS assumes you sold the oldest coins first. In our example, FIFO would force you to recognize the $40,000 gain. Many taxpayers accidentally use FIFO because their exchange reports it that way, leading to unexpectedly high tax bills.

If you want to use Specific Identification, start tracking your tax lots now. Use software that tracks your purchases and allows you to tag sales to specific buy orders. Without this, you are stuck with FIFO.

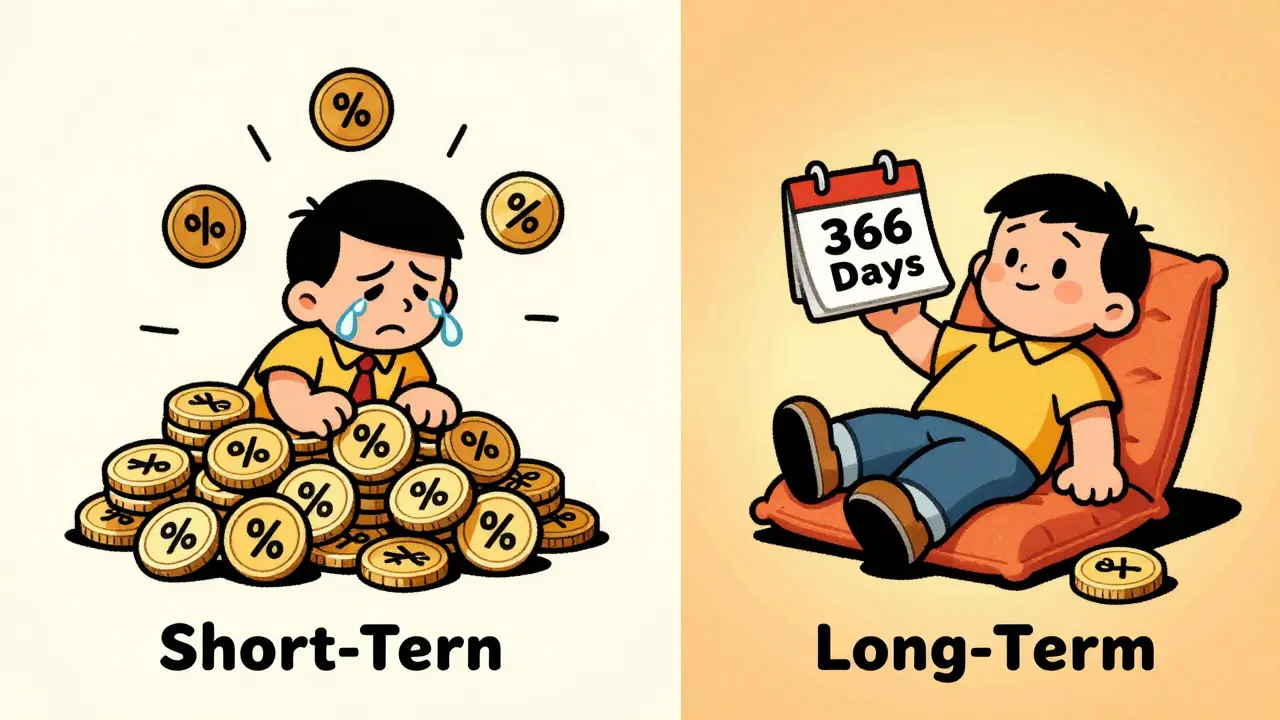

Capital Gains Rates: Short-Term vs. Long-Term

If you hold Bitcoin as an investment, your tax rate depends on how long you held it before selling. This is the biggest lever you have for tax efficiency.

Short-Term Capital Gains: If you sell Bitcoin you held for one year or less, the profit is taxed as ordinary income. This means it gets added to your salary and other income, potentially pushing you into a higher tax bracket. For high earners in 2026, this could mean paying up to 37% in federal taxes alone, plus state taxes.

Long-Term Capital Gains: If you hold Bitcoin for more than one year, you qualify for preferential rates. These rates are based on your total taxable income:

| Filing Status | 0% Rate Threshold | 15% Rate Range | 20% Rate Threshold |

|---|---|---|---|

| Single | Up to $47,025 | $47,026 - $518,900 | Above $518,901 |

| Married Filing Jointly | Up to $94,050 | $94,051 - $583,750 | Above $583,751 |

| Head of Household | Up to $63,000 | $63,001 - $551,350 | Above $551,351 |

If you earn less than $47,025 (single) or $94,050 (married), you might pay zero federal tax on your long-term Bitcoin gains. That is a powerful incentive to hold your assets for at least 366 days.

Special Events: Hard Forks and Airdrops

Bitcoin doesn't just exist in a vacuum. Sometimes, networks split, or new tokens appear in your wallet. These events have specific tax rules that often confuse users.

Hard Forks: A hard fork occurs when a blockchain splits into two separate chains. If a hard fork happens but you do not receive any new cryptocurrency units, there is no taxable event. You simply continue holding your original asset.

Airdrops: However, if that hard fork results in you receiving new coins (an airdrop), the IRS considers this ordinary income. You must report the fair market value of those new coins on the day you received them. "Receipt" is defined as the moment you have dominion and control over the coins-meaning you can transfer, sell, or trade them. Your cost basis for these new coins starts at the value you reported as income.

For example, if you receive 10 new tokens worth $5 each during an airdrop, you report $50 as ordinary income. If you later sell those tokens for $10 each, you have a $50 capital gain. If you sell them for $3 each, you have a $20 capital loss.

Record Keeping: Your Best Defense

The complexity of treating crypto as property makes record-keeping non-negotiable. The IRS expects you to track every transaction. This includes:

- Date of acquisition

- Purchase price (cost basis)

- Date of disposal

- Sale price or fair market value at time of transaction

- Purpose of the transaction (e.g., investment, payment for services)

Many taxpayers rely on specialized cryptocurrency tax software to automate this process. While the IRS does not endorse any specific tool, using reputable software can help generate the necessary forms, such as Form 8949, which details your capital gains and losses. Manual tracking is possible but prone to error, especially for active traders with hundreds of transactions.

Remember, the burden of proof is on you. If the IRS audits your return, you need to show the math. Keep screenshots of transactions, export data from your exchanges, and store everything securely. Digital wallets should also be documented, including private key holdings if applicable, to prove ownership and timing.

Common Pitfalls to Avoid

Even experienced investors make mistakes. Here are a few common errors that lead to penalties:

Ignoring Small Transactions: Just because you swapped $10 worth of Bitcoin for another coin doesn't mean it's not taxable. Every transaction counts. Aggregating small trades can add up to significant gains.

Misclassifying Income: If you accept Bitcoin as payment for freelance work, that is ordinary income, not a capital gain. You must report the value of the Bitcoin on the day you received it as wages.

Assuming Like-Kind Exchange Applies: Before 2018, some argued that swapping one crypto for another was a like-kind exchange under Section 1031, deferring taxes. The Tax Cuts and Jobs Act eliminated like-kind exchanges for anything other than real estate. Swapping Bitcoin for Ethereum is fully taxable today.

Failing to Report Foreign Wallets: If you hold Bitcoin on a foreign exchange or wallet, you may have additional reporting requirements, such as FBAR or Form 8938. Ignoring these can result in severe penalties unrelated to income tax.

What Comes Next?

The landscape of crypto regulation continues to evolve. The GENIUS Act of 2025 brought clarity to stablecoins and consumer protections, but it left the IRS's property classification intact. The CLARITY Bill, pending in the Senate, aims to further define regulatory boundaries but has not proposed changing the tax code's treatment of digital assets.

Until Congress passes legislation explicitly reclassifying Bitcoin as currency, the property rule stands. This means you should plan your investments with tax efficiency in mind. Hold for the long term to benefit from lower capital gains rates. Track your costs meticulously to avoid FIFO surprises. And when in doubt, consult a tax professional who specializes in digital assets. The rules are complex, but understanding them puts you in control of your financial future.

Is Bitcoin taxed as income or capital gains?

It depends on how you acquired it. If you bought Bitcoin to invest, profits are taxed as capital gains. If you mined Bitcoin or received it as payment for services, it is taxed as ordinary income at your marginal tax rate.

Do I pay taxes if I just hold Bitcoin?

No. Holding Bitcoin is not a taxable event. You only owe taxes when you dispose of it by selling, trading, or spending it. Simply watching the price go up or down does not trigger a tax liability.

What happens if I lose my Bitcoin due to theft or hacking?

You may be able to claim a casualty loss deduction. However, the rules for deducting crypto losses are strict. You must prove the loss was due to theft or casualty and that you took steps to recover the funds. Consult a tax advisor to ensure proper documentation and filing.

Does the GENIUS Act change how I pay taxes on Bitcoin?

No. The GENIUS Act, enacted in July 2025, focuses on regulatory oversight and consumer protection for stablecoins and digital asset providers. It does not alter the IRS's classification of Bitcoin as property or the existing tax reporting requirements.

Can I offset Bitcoin gains with losses from other stocks?

Yes. Capital gains and losses from Bitcoin can be netted against gains and losses from other investments like stocks or bonds. If your total losses exceed your gains, you can deduct up to $3,000 of the excess loss against your ordinary income per year, carrying forward any remaining losses to future years.